Ronald Woessner This is a reprint of an article originally published by equities.com here.

The benefits[2] of being a public company typically include

- Obtaining a source of permanent capital, usually at a cost lower than other alternatives,

- Providing early-stage investors an exit, allowing them to reallocate their capital and talent to other ventures,

- Attracting and retaining employees by providing equity-based compensation in the form of options and stock grants and an opportunity to monetize this equity by selling into the public market,

- Providing a stock “currency” that can be used for acquisitions.

While these benefits are, in theory, available to all public companies, as a practical matter these benefits are NOT available to the estimated 40% of smaller-cap NASDAQ issuers and the estimated 95+% of smaller-cap OTC-traded companies whose stocks are illiquid. These benefits are NOT available because:

- Investment firms are typically reluctant to invest in a company with an illiquid stock,

- Companies with illiquid stocks either attract no investment firm capital or toxic capital,

- If a company’s stock is illiquid, it is difficult for early investors to exit their investment position by selling shares in the open market,

- Equity-based compensation has little value to an employee if the employee is not readily able to convert the equity into cash by selling the equity in the open market,

- The shareholders of an acquisition target are typically unwilling to accept the acquiring company’s shares rather than cash as the “deal” consideration if they are unable to readily “monetize” most if not all of the shares by selling them in the open market.

Point being: smaller-cap companies with illiquid stocks are incurring the burdens of public company status and receiving NONE of the benefits. It’s no surprise that they are avoiding the public markets as illuminated in an earlier article of mine. As noted in this article, the disappearance of the smaller IPO (< $50M – $100M) is virtually 100% responsible for the declining number of public companies in America.

See below the FOUR Harvard Kennedy School Policy Recommendations to encourage more smaller-cap companies to go public.

- Increase the Threshold for Eligibility as a Smaller-Reporting Company and Non-Accelerated Filer

Companies that have more than $75M in market cap are required to file their quarterly and annual disclosure reports within 45 days and 75 days, respectively, of the end of the reporting period. They are also required to comply with Sarbanes-Oxley (“SOX”) Section 404(b), which requires an auditor attestation of the effectiveness of the company’s internal controls – this attestation is a major cost for small companies.

The HKS Policy Recommendation is to increase the $75M threshold to a materially higher number. A company with a market cap of only $75M is a TINY company by capital market standards. An issuer typically is not considered even to be a “small-cap” company until it has a market cap of $300M (and some say not until its market cap is $500M). Increasing the threshold would provide these tiny companies additional time to prepare their quarterly and annual filings. It would also exempt them from complying with the expensive SOX 404(b) internal control auditor attestation. SEC Chairman Jay Clayton has directed the SEC staff to consider increasing the $75M threshold.[3]

- Extend to 10 Years the Emerging Growth Company “On-Ramp” Exemption.

“Emerging growth companies” (“EGC”) who “go public” are currently permitted to operate for five years under lighter disclosure regulations, including NOT being required to comply with the SOX 404(b) internal control auditor attestation.[4]

The HKS Policy Recommendation is to extend from five years to 10 years the lighter disclosure period. Increasing the five-year “on-ramp” to 10 years provides EGC companies contemplating an IPO more confidence that they will have sufficient time to meet the enhanced regulatory requirements after becoming public.

H.R. 1645, the “Fostering Innovation Act” included in the JOBS 3.0 legislation approved by the House of Representatives earlier this year (but not yet approved by the Senate), extends the lighter disclosure period to 10 years.

- Increase the Shareholding Required to Demand Inclusion of Shareholder Proposals in Proxy Statements.

Current law permits a shareholder who owns as little as $2,000 of a company’s stock to demand that the company include the shareholder’s proposals for vote in the company’s proxy statement for the company’s annual shareholder meeting.[5] The $2,000 shareholding amount was created more than 30 years ago and is not fit for the present day.

- Shareholder proposals consume significant time and company resources to deal with, yet they cost almost nothing for shareholders to submit. A Manhattan Institute study found that in 2016, one-third of all shareholder proposals were brought by just six individual investors. This suggests that the proposals are being instigated by activist investors to promote social policy agendas, rather than to effect a bona-fide corporate governance purpose. Moreover, a proponent is allowed to resubmit a proposal on multiple occasions even if the proposal was previously rejected by a vast majority of shareholders.

The current system of shareholder class-action litigation is viewed by many as a mechanism to redistribute wealth from the insurance carriers, on the one hand, to the plaintiff and defense securities bar, on the other hand. Public companies and their insurers paid $55.6 billion in shareholder class-action settlements in the last 10 years.

In 2016, plaintiff’s attorneys received $1.27 billion in fees and expenses from such cases, out of the $6.4 billion in settlements.[6] Defense attorneys collect substantial fees and expenses to defend these claims as well. Very rarely, if ever, do these cases proceed to trial and they are typically settled (which enables the plaintiffs’ attorneys and defense attorneys to collect hefty fees) within the insurance policy limits.

One metric that illuminates the plaintiff attorneys’ “shakedown” character of many of these lawsuits is the frequency with which three law firms file shareholder class action lawsuits. These three law firms in 2016 filed 66% of the shareholder class action lawsuits and filed over 50% of the lawsuits during 2014 – 2017.[7] In 2016, these three firms were appointed lead counsel 36% of the time.[8]

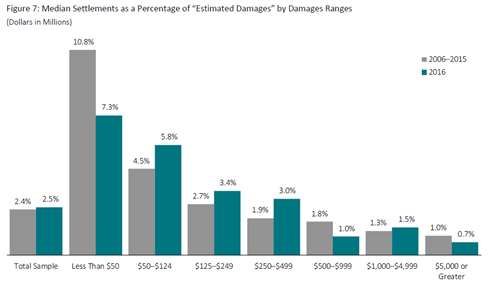

Another metric that illuminates the “shakedown” character of many of these lawsuits is the “algorithmic” calculation of the anticipated settlement amounts. The chart below shows the predicted settlement amount as a percentage of the claimed damages amounts:[9]

The plaintiffs’ law firms know these predicted settlement amounts before they file their lawsuits – hence, they can predict before filing the suit to a reasonable degree of certainty their estimated fees once the case settles – which as noted above, virtually all of them do.

Since 2006, the Committee on Capital Markets Regulation has urged the SEC to allow corporations to include in their charters a provision requiring mandatory arbitration of issuer-stockholder disputes. [10] Former SEC Commissioner Michael Piwowar in July 2017 endorsed this as well.

The HKS Policy Recommendation is to permit companies to require that shareholder class action litigation be settled via arbitration, rather than litigation.

With arbitration, these matters can be resolved quicker and less expensively. Also, arbitration is seen as a mechanism to discourage specious or flimsy claims from being brought in the first instance – often only for the purpose of obtaining quick cash settlement from companies (and their insurers) who want to avoid the cost and management distraction of the litigation.

These were the FOUR HKS Policy Recommendations to encourage more companies to go public. While excellent suggestions, they do NOT address the root cause of the inhospitality of the public markets to smaller-cap companies.

Stay-tuned for a completely NEW policy recommendation, credited to David Weild IV, who is widely reported as being the “Father of JOBS Act 1.0,” to combat the “disappearing US public company” phenomena. This NEW policy recommendation will be illuminated in a subsequent article.

© Ronald A. Woessner, December 18, 2018

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++

Mr. Woessner mentors, advises, and raises capital for companies in the start-up and smaller-cap company ecosphere. He also advocates in Washington DC for policies to help smaller-cap companies access capital and for policies that create a more hospitable public company environment for them. See here for more information on Mr. Woessner’s background.

[1] Lux and Pead, “Hunting High and Low: The Decline of the Small IPO and What to Do About It, Mossavar-Rahmani Center for Business and Government, Harvard Kennedy School (April 2018). https://www.hks.harvard.edu/centers/mrcbg/publications/awp/awp86.

[2] Dell Computer shareholders recently approved the company (again) becoming a public company after five years as a private company.

[4] This is one of the provisions of the so-called 2012 “JOBS 1.0” law.87% of all IPOs since the enactment of JOBS 1.0 have been identified as emerging growth companies.

[5] If the company determines NOT to include the proposal, then the company is required to justify its decision.

[6] Scott, Hal. “Shareholders Deserve Right to Choose Mandatory Arbitration.” CLS Blue Sky Blog, Aug. 21, 2017,http://clsbluesky.law.columbia.edu/2017/08/21/shareholders-deserve-right-to-choose-mandatory-arbitration/.

[7]Cornerstone Research, “Securities Class Action Filings, 2017 Year in Review, at 35.

https://www.cornerstone.com/Publications/Reports/Securities-Class-Action-Filings-2017-YIR

[8] Id at 35.