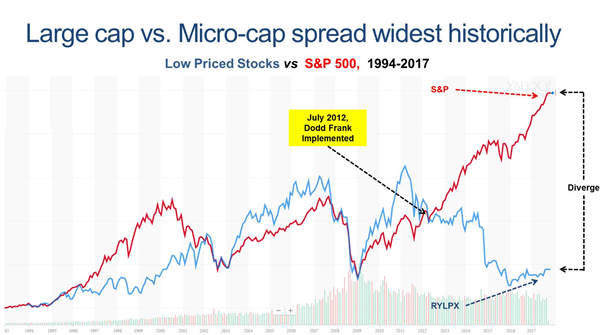

The chart above, excerpted from an article by noted financial analyst Michael Markowski, who predicted the demise of Lehman, Bear Stearns and Merrill Lynch, appears to illustrate that the Dodd-Frank legislation crushed the values of smaller cap companies. Mr. Markowski’s article appears at this link: https://www.equities.com/news/dodd-frank-boon-for-large-caps-bust-for-micro-caps

Is this causation, or merely correlation? We don’t know for sure.

What we do know is that smaller cap public company valuations have diverged markedly from larger cap public company valuations, regardless of the proximate cause. As an investment asset class, they appear to have performed poorly.

Further, to add to the woes of the smaller cap public companies, we also know that the US public markets are generally* inhospitable to smaller cap companies. This inhospitability manifests itself as follows:

(1) Smaller-cap stocks are illiquid

(2) Institutional investors avoid investing in illiquid smaller cap stocks

(3) Smaller-cap companies have little-to-no investment analyst coverage

(4) Smaller-cap companies are starving for capital

(5) Much of the available capital to smaller-cap companies is “toxic”

(5) Gaps in SEC “short” selling regulations enable short sellers unfairly to damage smaller-cap company valuations and the companies themselves

We will review each of these elements of inhospitabililty in subsequent articles.

* Of course, there will be exceptions to the above general principles, particularly if the company is in the biotech or cannabis space.

Image: Amur leopard, a critically endangered species. Source:

World Wildlife Fund

According to a recent Forbes article, America ranks as the best

country for female entrepreneurship. That’s “good.” On the other

hand, the “bad” is that companies founded by women entrepreneurs are

less likely to be funded by a venture capital firm than the Earth being struck

by an asteroid, as I discussed previously in this space.

That’s “not so bad,” though. Women entrepreneurs are

not missing out on much by not being funded by venture capital firms =>

since venture capital firms fund only approximately five of every 10,000

startups in America, according to Entrepreneur.com.

The “worst,” news, however, is that women

entrepreneurs will join their male counterparts in struggling to raise capital

to keep their businesses alive because of the lack of investment capital for

start-up businesses in America as a whole.

This lack of investment capital for US start-up businesses is an

endemic problem. Like an invisible chain, it extends across the length and

breadth of the US and restrains an entire ecosystem, beginning with startups in

a garage, and extending to OTC Markets traded companies, and further extending

to smaller-cap publicly listed companies.

Without sufficient capital, these businesses fail.

Predictably, many would-be entrepreneurs decide to keep their

day jobs rather than taking the entrepreneurial leap when they see the

businesses of their friends, neighbors, or relatives go “out of business” and

the often-consequent loss of life savings and the family home.

With this background in mind, you might be thinking that fewer

and fewer Americans want to become entrepreneurs today than in previous years.

You are correct.

The data demonstrates that entrepreneurship in America is dying.

In February of this year, Mr. David Weild IV, “Father of JOBS Act

1.0,” former Vice Chairman of NASDAQ and New York investment banker, gave

a presentation at The Yale Club of NYC. The JOBS Act, signed into law by

President Obama in 2012, was a great start for the movement to level the

playing field for emerging growth companies, but even Mr. Weild will tell you

that more needs to be done.

The presentation included a “heat” map, derived from

Census Bureau statistics of US business formations by state per capita. The

heat map shows business startups by state, per capita, in 2006 versus 2017. In

2006, the map shows much of the US as dark red, connoting high numbers of

startups per capita. Disturbingly, in 2017, the map shows much of the US as

pale pink, connoting a paucity of startups.

Business Formations within 4 Quarters by State – Per 1,000

People

And, while entrepreneurship in America is dying, so are the US public markets according to some. Others say the public markets are inhospitable to smaller cap companies or that the public markets are “broken.” Regardless of the choice of words, the US public capital markets are no longer the envy of the world, as they once were. To wit:

(1) 3,500 (40%) of the approximate 8,700 NASDAQ/NYSE trading

symbols (mainly smaller-cap issuers) have average daily trading volumes under

50,000 shares per day, and approximately 50% had volumes under 100,000 per day,

according to the SEC.

(2) There are approximately 50% fewer public companies today

than 20 years ago.

(3) The number of book runners for smaller IPOs (<$100

million in proceeds) has decreased from 162 in 1994 to 31 in 2014.

Americans are struggling. The US public markets are dying.

Entrepreneurship is dying. It’s time for Congress or the SEC, or both, to adopt

pro-capital formation policies before matters continue to get worse. If not

remediated, the US will forfeit its position as the financial capital of the

world. And, that would be really, really bad.

More on this topic to follow.

Article originally published on November 25, 2019 by equities. com here.

The probability of planet Earth having a catastrophic collision with an asteroid is higher than the probability that a startup founded by all women will be funded by a US venture capital firm.

Startling, isn’t it? Read on.

According to the entrepreneur.com article here, as seen in the chart below, venture capital firms fund about 0.05% (1/20 of 1%) of US startups.

1 Excludes ICOs. 2 According to the article here of StartEngine, one of the largest equity crowdfunding portals, as of February 2019, since inception only $176 Million has been raised via crowdfunding. In comparison, venture capital firms funded $130.9 billion across 8,949 US companies in 2018!

As

recently widely reported, for example in the article here, of these

1/20 of 1% of startups funded by venture capital firms, only 2.5% have all women

founders.

So

according to the math:

0.0005 * 0.025 = 0.000125 of startups in

America will have all women founders and will be funded by venture capital

firms, or 1.25 of every 10,000 startups.

In comparison, the odds of the earth having

a catastrophic collision with an asteroid in the next 100 years may be as high

as 1 in 5,000 according to the

article here.

As revealed with a little more math,

1/5000

= 0.0002 odds of the earth having a catastrophic collision with an asteroid in

the next 100 years

1.25/10,000

= 0.000125 odds of an all-women start-up being funded by a venture capital firm

0.0002/0.000125

= 1.6

In sum, the earth is 1.6 times more likely to have a

catastrophic collision with an asteroid in the next 100 years than a start-up with

all women founders is to obtain funding from a venture capital firm!

As amusing as some may find the above comparison, it’s really quite a serious problem for America. Female human capital is simply not being given the opportunity to succeed. American entrepreneurship is stymied, tens of thousands of US jobs are lost, upward mobility is choked, and the US economy and future economic growth are being stunted — of of which, if left unchecked, will one day result in the US losing the current battle with China for worldwide technology dominance.

And, if you are a woman of color – the odds of securing venture funding approach zero. According to Ms. Kapin, only 0.0006% of venture funding has gone to women of color since 2007. Applying this metric to the $130.9 billion in 2018 venture funding noted in the chart above, approximately $785,000 would have gone to firms founded by women of color. More information on the topic of funding to minority founders appears here, “Untapped Opportunity: Minority Founders Still Being Overlooked.

As noted in an earlier article of mine, US public policy is killing small business and entrepreneurship in America, keeping the poor “poor” and thwarting the American Dream of “Main Street” upward mobility: the US public capital markets, once the envy of the world, are in-hospitable to smaller-cap companies; US entrepreneurship is at historical lows[1]; on a GDP basis, the US surpassed only two of the world’s top 26 IPO markets — Mexico and Brazil — as to the number of smaller-cap company IPOs[2]; the Chinese are lapping the US in the number of total IPOs[3]; and millions of high-quality U.S. jobs have been forfeited.

To remedy this, a “big-tent,” bi-partisan, multi-racial, male/female coalition advocacy effort is being organized in Washington, DC. The coalition, named “JUMMP” (“Jobs, Upward Mobility, and Making Markets Perform”), is being spearheaded by David Weild, former Vice-Chairman of Nasdaq, New York-based investment banker, and “Father of JOBS Act 1.0.” Pro-entrepreneur and pro-upward mobility Americans, including me and others, from both sides of the political aisle in Washington, DC, and throughout the US, are helping Mr. Weild.

The JUMMP Coalition’s objectives are

to:

restore America’s capital markets to their former health,

create millions of US jobs,

help US entrepreneurs regardless of color and gender succeed,

reverse the increasing income inequality trend,

reinvigorate the American Dream of upward mobility from one generation to the next,

bring millions of Americans, especially minorities and others who have not realized the financial benefits of the US economic expansion, to the metaphorical “mountain top,” and

assure the US maintains its worldwide technological dominance

In the meantime,

until the JUMMP Coalition achieves these objectives, if you are a woman founder of a startup and your

business plan requires venture capital funding – it would probably be best if

you have a backup plan.

[This is a reprint of an article published by equities.com here.]

+++++++++++++++++++++++++++++++++++++++++++++++++

[1] Unpublished White Paper of David Weild, former Vice-Chairman of Nasdaq, New York-based investment banker, and “Father of JOBS Act 1.0.” A “heat map” included in Mr. Weild’s White Paper shows that the number of start-ups in America in 2017 versus 2006 in the vast expanse of Middle America between the East and West coasts has decreased by approximately 50%.

[2]

“Making Stock Markets Work to Support

Economic Growth,” Weild, Kim & Newport for the OECD, July 11, 2013, at

p. 54. For the period from 2008-2012 the U.S. had a disastrous “Efficiency

Ratio” of GDP-weighted output of small IPOs — at only 0.4 IPOs per $100

billion of GDP (ahead of only Mexico and Brazil).

[3] According to Mr. Weild’s research, the number of public companies in China has increased by 381% since 1997, while the number of public companies in the US has decreased by 39%.

+++++++++++++++++++++++++++++++++++++++++++++++++

Mr. Woessner mentors, advises, and helps companies in the start-up and smaller-cap company ecosphere raise capital through Regulation Crowdfunding (CF) and other means, bringing to bear his 25+ years of experience in the smaller-cap, public company ecosphere as CEO and general counsel. He also advocates in Washington DC for policies that create a more hospitable public company environment for smaller-cap companies, enhance capital formation, support small business, promote entrepreneurship, and increase upward mobility for all Americans, particularly minorities. See herefor more information on Mr. Woessner’s background.

Ronald Woessner This is a reprint of an article of mine originally published by equities.com at the link here.

+++++++++++++++++++++++++++++++++++++++++++++++++

Public Policy is Killing Stock Markets for Smaller-Cap Companies

US Public policy has caused the well-publicized and alarming decrease in the number of US publicly-listed companies and is poisoning the public markets for smaller-cap companies.[1]

The number of US publicly-listed companies

decreased over the last two decades by about 44%, from 8,823 in 1997 to 4,916

in 2012, according to the World Federation of Exchanges. A 2018 academic study from the Harvard

Kennedy School reveals similar numbers.[2]

Other countries are lapping the

US in the number of their public company listings versus our public company

listings. During the comparable period in other developed countries, public

listings increased by about 48%.[3]

The US “should have”

approximately 10,000 public companies today, resulting in an estimated

“listing gap” of approximately 6,000 companies.[4]

This

decrease should be shocking and frightening to all Americans, regardless of

party affiliation, particularly when one considers that real GDP has grown by

over 60% in that time frame. Why, when our economy is growing strongly, has our

public listing machine come to a grinding halt?

This

decrease has cost America tens of millions of jobs,[5]

reduced to a mere trickle the queue of future “Fortune 500” larger-cap

companies for Fidelity, CalPERS and hundreds of pension plans to invest in,[6]

and puts the US on the vector of falling behind China in China’s quest to

dominate the US technologically.[7]

Here’s the chain of causation that’s created the US Listing Gap:

Step 1: The introduction of electronic trading

execution, order handling rules, and smaller tick sizes collapsed buy/sell

trading spreads to $.01 from $.25 per share and collapsed retail sales

commissions to $5.00 per trade from $250 per trade.[8]

Step 2: These smaller bankable

spreads and reduced retail sales commissions DRASTICALLY reduced the

profitability (i.e., ability to make

money) of smaller and mid-size broker dealers. This drove 74% of IPO

bookrunners out of business[9] and drove 29% of

broker-dealers out of business.[10] Those remaining eliminated the investment

banking, research, retail sales, and capital committed to market making (i.e., creating stock trading liquidity) they

previously provided for smaller-cap companies.[11]

Step 3: Lack of this

“after-market” support from smaller and mid-size broker dealers has

left thousands of smaller-cap companies as public-company “orphans,”

with no broker-dealer or investment-banking sponsorship, and poisoned the public

markets for smaller-cap companies.[12]

Step 4: This

in-hospitability deters smaller-cap companies from conducting IPOs and going

public. The big investment banks discourage these smaller deals with smaller stock

trading “floats,” as they are difficult to market to their most

actively trading institutional clients. They are also difficult transactions

purely from an ROI and opportunity cost perspective of allocated resources.

Step 5: This disappearance of the smaller-cap

company IPO (< $50M) is predominantly responsible for the US Listing Gap

according to academic research and as stated by former SEC Commissioner Michael Piwowar during his

opening remarks at an SEC – NYU conference on IPOs in May 2017: “The

substantial drop in the number of IPOs in the United States is primarily driven

by the disappearance of small IPOs.”

Former Commissioner Piwowar is correct.

The number of IPOs raising less than $100 million collapsed starting in 2000.

The number of these small IPOs averaged 401 annually in the 1990s, but then

dropped to only 105 annually in the 18 years since. In the 1990s, small IPOs

represented 27% of all capital raised in the public markets, whereas in the

period from 2000 to present they have represented only 7% of all capital

raised.[13] Moreover, according

to an OECD study, during 2008 – 2012 on a GDP weighted basis the US was

third from the bottom for small IPOs among 26 countries studied — ahead

of only Mexico and Brazil.[14]

The electronic execution, order handling

rules and $.01 tick size trading rules created the salutary benefit of reducing

stock trading transaction costs. Nevertheless, they also had the unintended

negative consequence of killing the small-cap IPO and creating the currently

poisoned US public markets for smaller-cap companies. As eloquently stated by David

Weild,

former NASDAQ Vice-Chairman, Wall Street investment banker, father of JOBS Act 1.0,

and tireless advocate for the health of the US

capital markets:

“Why

have smaller-cap company IPOs disappeared? Because the profitability of the

investment banking-focused broker-dealers —

which previously sponsored and fostered a habitable environment for

smaller-cap companies through underwriting, distributing and supporting them in

the after-market via sales, research, and market-making (capital commitment) —

has been destroyed by electronic-order execution, small-tick-size markets,

that make it easy for predatory short-sellers to collapse trading spreads

(especially in advance of offerings) and spread lies to drive down stock prices

that cannot be countered because the investment banks that remain can no longer

afford to provide research and sales coverage to counteract the lies.”[15]

Through the “butterfly effect,”[16] the electronic execution,

order handling rules and $.01 tick size trading rules had the unintended

consequences[17]

of:

killing the

smaller-company IPO market,

causing the loss

of tens of millions of US jobs,

forcing businesses

to close because of lack of capital,

discouraging

entrepreneurship,

hindering upward

mobility for all Americans, especially minorities

destroying the

efficacy of the US capital markets, and

creating an

opportunity for the Chinese to technologically dominate the US.[18]

Who

would have thought that the lack of a few pennies in tick size would have

poisoned the US public capital markets, once the envy of the world?[19]

So,

what is to be done to remedy the current in-hospitability of the public markets

to smaller-cap issuers, which is causing them to avoid the US public market?

Let’s

use our common sense to intuit the policy solution. Since the $.01 bid/ask tick

size is a root cause of the current inhospitably of the public markets to

smaller-cap companies, then one would naturally think that increasing the tick

size to some larger number would remedy the issue.

And,

indeed, academic research demonstrates this to be precisely the case!

The

academic research of Mr. Weild and his colleagues demonstrates that widening

tick sizes for smaller-cap illiquid stocks results in more smaller-cap

companies going public. In

other countries where there are higher tick-sizes-as-a-percent-of-share price (which

in turn leads to higher bid-ask spreads) their smaller-cap IPOs are booming.

There is a nearly 70% correlation between tick-sizes greater than 1% of an

issuer’s trading price and a robust IPO market for companies under $500 million

in market value, according to the research.[20]

Now, a word about the two year 2016 – 2018

SEC tick

pilot study.[21] The study increased the tick size from $.01

to $.05 for the pilot stocks. It has been reported that the study was a

“failure” because it cost investors approximately $350M more to trade

the pilot stocks during the study period and did not produce the hoped-for and

anticipated increase in the trading liquidity of the pilot stocks.[22] Commentators have

incorrectly concluded from these reports that larger tick sizes and larger bid-ask spreads do not increase trading liquidity.

These

commentators are incorrect. The failure of the tick pilot study to produce the

hoped-for and anticipated increases in trading liquidity of the pilot stocks is

100% attributable to the inherently flawed design of the study.[23]

The

study design was inherently flawed in that that

there was a null set (i.e., ZERO) of stocks

in the pilot that could benefit from the tick pilot. The explanation

appears below.

Recall that the academic research says the

tick size must be > 1% of the stock share price. The $.05 tick was not >

1% for those stocks priced > $5.00 per share. The $.05 tick was > 1% for those stocks

priced < $5.00 per share … but broker-dealers cannot recommend them for

purchase because of brokerage firm policies[24] and such stocks cannot be

purchased on margin.

Since the study design

was inherently flawed to benefit ZERO issuers, it’s not surprising that ZERO

issuers benefitted.

In

conclusion, it is clear what needs to be done from a policy perspective to

remedy the poisoned and collapsing US public capital markets: create a special

exchange with special trading rules for smaller-cap issuers that permit higher

bid-ask spreads.[25]

These

higher bid-ask spreads will then create the profitability broker-dealers need

to begin again providing after-market

“sponsorship” and support for smaller-cap companies in the form of:

investment

banking,

investment analyst

research,

providing retail sales persons to solicit customer buy orders, and

committing capital

to make a trading market in the issuer’s stock

These

activities would in turn make the public capital markets more hospitable to

smaller-cap companies, which in turn would motivate more of them to go public,

and would enable those that are already public to thrive.

A

big-tent, bi-partisan advocacy effort is now being organized in Washington, DC,

to present this initiative to Congress and to the SEC. If you want to help:

restore America’s capital markets to their former health,

create millions of US jobs,

help America’s entrepreneurs succeed,

promote upward mobility and bring millions of Americans, especially minorities and others last hired during an economic recovery, to the metaphorical “mountain top,” and

assure the US maintains its worldwide technological dominance

[1] There are approximately 5,500 “publicly-listed” companies listed on the NYSE and NASDAQ. There are another approximately 10,500 “OTC-traded” companies. The term “public markets” as used in this article refers collectively to both publicly-listed and publicly-traded companies.

[2]“Hunting High and Low: The Decline of the Small IPO and What to Do About It,” Lux and Pead, Mossavar-Rahmani Center for Business and Government, Harvard Kennedy School (April 2018), https://www.hks.harvard.edu/centers/mrcbg/publications/awp/awp86 (hereinafter cited as “Lux & Pead”). The World Federation of Exchanges number of publicly-listed companies as of December 2018 is 5,343. There appears to have been a modest uptick resulting from JOBS Act 1.0 and JOBS Act 2.0 and the robust economy.

[3] 9,538 is the estimated “should have” number as of 2012 according to the study. “The U.S. Listing Gap,” Doidge, Karolyi, and Stulz, December 2015, at p. 8.

[4] The author

extrapolates to an estimated 10,000 “should have” number in 2019.

Other commentators peg the “should have” number of public companies

as > 13,000.

[5] It is estimated

that 22M jobs were lost between 1997 and 2010 because of the reduced level of

IPO activity. “A Wake-Up Call for America,” Weild & Kim, November

2009 (hereinafter cited as “Weild & Kim”), at p. 27.

[6] Today’s Fortune

500 companies were smaller-cap companies at one time. It’s necessary to have a public market

ecosystem that enables smaller-cap companies to thrive so that those

smaller-cap companies who have the potential to become a Fortune 500 company –

have a fighting chance to do so. Today’s

public market ecosystem is so inhospitable to smaller-cap companies that many

who have the potential to become a Fortune 500 company will never achieve their

potential.

[8] “Hearing on

Legislation to Further Reduce Impediments to Capital Formation,” Financial

Services Committee, on October 23, 2013, Statement of David Weild, at 15 – 16.

[9] As of 2012, there were only 44 IPO bookrunners still in business, down from 167 in 1994. Id.

[11] The $.01 bid/ask trading spreads

have (a) decimated the ranks of the small-to-mid size broker dealers/investment

banks who formerly provided after-market support for smaller-cap companies, (b)

eliminated virtually 100% of the retail salesmen who previously phoned retail

investors and solicited buy orders for a small-cap issuer’s shares of stock, and

(c) decimated the ranks of the sell-side investment analysts who left the

industry in droves to work for hedge funds and the like.

[13] Lux and Pead at

p. 8. A delta of 296 (401 – 105) * 18 years = 5,328, which predominantly

accounts for the Listing Gap.

[14] “Making Stock

Markets Work to Support Economic Growth,” Weild, Kim & Newport for the

OECD, July 11, 2013 at p. 54.

[15] “Fixing America’s IPO Markets, Why this is Essential for US National Interests, Ideas for JUMMP Act 1.0,” D. Weild, unpublished paper, February 2019.

[16] The butterfly effect is the phenomenon whereby a minute localized change in a complex system can have large effects elsewhere.

[18]Id. There is an additional network effect that magnifies the extent of this damage. Enrico Moretti at Berkeley in his book. “The New Geography of Jobs,” wrote about the “multiplier effect” of how a single high-tech job in an “innovation hub” like Boston, San Francisco, or Raleigh-Durham creates five new jobs in the surrounding service sector. Hence, all those IPOs that didn’t happen didn’t create a successful company that then didn’t hire people that then resulted in the communities not flourishing.

For want of a nail the shoe was lost. For want of a shoe the horse was lost. For want of a horse the rider was lost. For want of a rider the message was lost. For want of a message the battle was lost. For want of a battle the kingdom was lost. And all for the want of a horseshoe nail.

[20] “Making Stock Markets Work to Support Economic Growth,” Weild, Kim & Newport for the OECD, July 11, 2013, at p. 54. For the period from 2008-2012 the U.S. had a disastrous “Efficiency Ratio” of GDP-weighted output of small IPOs — at only 0.4 IPOs per $100 billion of GDP (ahead of only Mexico and Brazil). Why? Because the US has the lowest tick-sizes-as-a-percent-of-share price of any of the 26 countries studied. A number of countries enjoy 50x the GDP-weighted output of the number of small IPOs in the US. Id.

One

may ask: “How do we know this is causation and not merely

correlation?” Answer: because we have seen from our experience here

in the US how the lower bid/ask spreads created the loss of after-market

support for smaller-cap issuers. See note 12 above and the articles cited

therein.

[21] The SEC studied for two years the effects on the trading liquidity

of 1,200 NMS pilot stocks of widening the tick size from a penny ($.01) to a

nickel ($.05).

[22] Trading liquidity

is necessary for a public issuer to attract investment firm capital. As noted

by Weild & Kim and in earlier articles of mine: without trading liquidity a public issuer has

virtually zero chance of attracting non-toxic investment firm capital. See, e.g., https://www.equities.com/news/why-do-investment-analysts-ignore-smaller-cap-companies.

[23] Early proponents of the SEC study criticized the proposed

study design at the time it was being designed.

At the time, Mr. Weild and others stated that the study design

was flawed and not remotely close to the tick size pilot they had advocated

for. The Carney – Duffy legislation,

which would have required the SEC to conduct the pilot according to certain

parameters, called for a 5- year pilot (not 2 years) and a $.10-cent tick size

(not $.05). The legislation never became

law and hence the SEC did not follow these parameters in designing the study.

[24] Brokerage firm policies prohibit

brokers from calling customers to solicit a buy order for stocks priced at

<$5.00 per share.

[25] This is the fundamental requirement. Obviously, there are hundreds of other details as well that would be necessary for such a trading venue to function properly.

+++++++++++++++++++++++++++++++++++++++++++++++++

Mr. Woessner mentors, advises, and helps companies in the start-up and smaller-cap company ecosphere raises capital through Regulation Crowdfunding (CF) and other means. He also advocates in Washington DC for policies that create a more hospitable public company environment for smaller-cap companies, enhance capital formation, support small business, promote entrepreneurship, and increase upward mobility for all Americans, particularly minorities. See here for more information on Mr. Woessner’s background.

Readers — an earlier article of mine published by equities. com at this link discussed how smaller-cap US public companies are being hurt by not having research investment analysts covering their stock. As bad as the lack of investment analyst coverage is now for smaller-cap companies (and it is REALLY bad), matters will get MUCH worse if the European MiFID II is adopted in the US.

According to the Bloomberg article below, which originally appeared at this link, the European MiFID II directive has decimated the European investment analyst ranks. If adopted in the US, it would have an equally decimating effect on the US investment analyst community and create an even worse circumstance for US smaller-cap companies! +++++++++++++++++++++++++++++++++++++++++++++++++

Research Analysts’ Existential Crisis Enters MiFID II Era

Analyst headcount falls as EU rules put price on research

Merian’s Buxton says quality of research is deteriorating

Predictably, by putting a price tag on research, the European Union rules have made asset managers more selective about what they need, especially since most have opted to swallow research costs rather than pass them to clients. Many have also boosted their in-house analysis capabilities.

More Pressure

Consequently, there’s even more pressure now to write reports with concrete conclusions, rather than trimming estimates by 3 percent on a stock rated “hold,” said an analyst who manages a team and asked not to be identified discussing internal matters. Another analyst who also requested anonymity said calls on a stock are now more important than long-term thematic pieces. Anthony Codling, an analyst at Jefferies LLC who quit recently, said he reduced the amount of what he deemed “maintenance research.”

“Why would a client pay to receive a note that says results are in line?” he said.

Those concrete conclusions are sometimes drawing rebuttals from companies. U.K. real estate services company Purplebricks Group Plc in February disputedCodling’s analysis of its accounting, while lab-testing company Eurofins Scientific SE said “factually wrong estimates” from Morgan Stanley’s Edward Stanley may have misled or confused investors. French grocer Casino Guichard-Perrachon SA contested research by Bernstein’s Monteyne.

Of course, many analysts would say research always should have had demonstrable value, even before MiFID II; what’s new is the intensifying competition for payments. But some lament that a new model that measures clicks and analyst interactions by the hour ignores the subjective quality of analysis.

While there have been murmurs about a supposed sensationalist turn in investment research, the caliber of analysts also is declining, meaning that one still sees meaningless reports, said Richard Buxton, chief executive officer of fund manager Merian Global Investors — such as when a brokerage says the outlook for the mining sector is increasingly a macro call.

Shrinking Coverage

“The quantum of coverage is shrinking, the quality of coverage is definitely shrinking, and it’s no surprise therefore that we are continuing to pay less and less for the research,” he said from London. “We know good people are leaving the sell side, and that has to be a consequence of [the fact that under] MiFID II people are not going to earn the same amount of money as they used to as a research analyst.”

Headcount for equity research at 12 major investment banks has declined 14 percent since 2013 to 1,200 as of the first half of 2018 in Europe, the Middle East and Africa, data from Coalition Development Ltd. show. Over the same period, the number of ratings on companies in the Stoxx Europe 600 Index has dropped 9 percent while the number on the Stoxx European small-cap index has fallen 12 percent, according to data compiled by Bloomberg.

To Robert Miller, head of research at Redburn, the biggest risk to the industry is the attrition of talent.

Talent Pool

“Because of the deflation in the industry, the risk is that the best talent decides that they really need to work on the buy side or in the industry or do something completely different,” he said. “The pool of high-quality, experienced talent in my industry is shrinking.”

The industry is seeing more mergers as revenue falls. AllianceBernstein Holding LP, the asset manager that owns Sanford Bernstein, agreed in November to buy Autonomous Research, which specializes in financial stocks. Germany’s MainFirst Holding AG last month took over Raymond James Financial Inc.’s institutional brokerage business in European stocks. U.S. securities firm Stifel Financial Corp., in turn, is buying MainFirst’s equity research and brokerage operations.

Research houses are also exploring new sources of revenue. More are now charging companies for reports about them — a “sponsored research” model that has spurred worries of conflicts of interest. Some firms say companies are paying larger retainers for brokerage services including research. One, French firm AlphaValue SA, is asking investors to “crowdfund” analyst reports.

Metrics-Driven

Regardless, investment research — an area of finance that can seem almost academic at times — is becoming more metrics-driven. Many banks now charge explicitly for meetings and calls with analysts, making investors more selective about such conversations. These interactions are now recorded for compliance, with their value scored by the user.

“The battleground is interaction between research analysts and the buy side, who are increasingly adopting the accountant or legal industries’ ‘gas meter’ model of by-hour pricing,” said Ed Allchin, head of sales and business development at Autonomous Research in London. “This has made fund managers more reluctant to contact analysts because they may be charged each time, with thought going in to the economics of that call or meeting.”

Gone are the days when investors would meet with analysts casually just because they happen to be in the area. There are now fewer ad-hoc meetings and more that are focused on specific subjects, said Redburn’s Miller, even though the research firm doesn’t charge by the hour. The number of calls fell at the start of the year, but has since recovered, said Bernstein’s Monteyne.

Still, the realities differ for different research providers. Large investment banks can afford to sell analysis at lower prices, since it’s just one part of a large business. Independent research houses do not have that advantage but can tout their conflict-free specialization. The jury is still out on who will ultimately emerge victorious, but increasingly the worry is that the smaller players will drown.

Market Impact

For investors, the concern is that shrinking analyst coverage, especially in small- and mid-caps, will make the market less efficient, with lower liquidity, though some say that could help active stock pickers. Already smaller companies are feeling the pressure to beef up investor relations resources, as they can no longer count on analysts alone to tell their story.

The rules may be amended. European regulators are studying their impact, including on smaller stocks and independent research providers. U.K. regulators will step up scrutiny of falling pricing models and research budgeting, while elsewhere in Europe, rules may be softened to lessen the blow on smaller companies, Bloomberg Intelligence said in a note on Thursday.

But little is likely to reverse the existential crisis in research. For an industry that thrives on dissecting numbers and predicting winners and losers, it makes sense that its value and future should now determined by market forces.

“Investment research is a declining industry given the cost pressures,” said Ian Harnett, who left UBS in 2006 to start macro analysis firm Absolute Strategy Research Ltd. “If you survive through that process than maybe there is an opportunity to increase your market share. What we do not know is what the value of that market share will be in three years’ time.”

+++++++++++++++++++++++++++++++++++++++++++++++++

Mr. Woessner mentors, advises, and helps companies in the start-up and smaller-cap company ecosphere raise capital. He also advocates in Washington DC for policies that create a more hospitable public company environment for smaller-cap companies, enhance capital formation, support small business, promote entrepreneurship, and increase upward mobility for all Americans, particularly minorities. See here for more information on Mr. Woessner’s background.

This article explains how smaller-cap companies with illiquid stocks can create sustained, significant trading volumes with investor relations (“IR”) firms, thus enabling them to attract investment firm capital and investment analysts. Sustained, significant trading volumes are necessary to attract investment firm capital and investment analyst coverage, as illuminated in earlier articles of mine.[1]

CEOs of smaller-cap companies with illiquid stock trading volumes often ask me, “How do I create sustained, significant[2] trading volume in my company’s stock?”

The answer is simple. The company needs to attract Main Street (retail) investors, rather than Wall Street (investment firm) investors. When enough retail investors begin buying and selling a company’s stock, the trading volume will increase to a sufficient level such that an investment firm will consider making an investment in the company.[3]

Attracting retail investors typically requires your company to hire an IR firm to perform “market awareness” activities, i.e., efforts directed to informing potential Main Street investors of the opportunity to purchase the company’s stock through the open market.

Company CEOs also often ask me: “Why is it necessary to hire an IR firm to get “more eyes” on my company’s stock; isn’t producing excellent financial results, or having a unique product, or having a compelling business model, or having a huge market opportunity, etc. – isn’t that enough to attract Main Street investors?”

The answer is … “No – that’s typically not enough. Sorry.”

Think of it this way. There are approximately 15,000 publicly-traded companies in the US, including those traded through the over-the-counter (OTC) market. Common sense suggests that the average Main Street retail investor is NOT going to find your company’s stock from among these 15,000 companies without your company implementing targeted, effective initiatives to “market” your stock to retail investors.

Of course, there are companies that do not have to implement stock marketing campaigns to attract retail investors: some CEOs are well-known and have a public following, or the company otherwise has become known to the investing public, or the company is in a “hot” investment sector (biotechnology, cannabis, etc.). The reality of the capital markets is this: a company that does not fall into these categories must implement targeted, effective initiatives to “market” its stock to Main Street investors and motivate them to purchase the company’s shares through the open market in order to achieve sustained stock trading liquidity. Period. Paragraph. End of discussion.

The next questions invariably are: “What exactly do investor relations firms do, anyway?” and “What initiatives are effective in marketing an illiquid company stock to Main Street investors to create sustained, significant stock trading liquidity?”

The services performed by investor relations firms often vary from firm-to-firm. The services typically performed by investor relations firms appear below: some firms perform all of these tasks, while some perform only a few.

Designing that portion of the company’s web site that is directed toward investors. (That portion typically resides under a tab named “Investors Relations.”)

Writing the script for investor conference calls.

Introducing the company to potential investors via one-on-one meetings or via group meetings at breakfasts, luncheons, etc.

Sending the company’s press releases to the IR firm’s “proprietary” distribution list of potential investors.

Phoning potential retail investors and asking them if they would be interested in receiving information about the company.

Implementing social media and digital campaigns about the company directed to retail investors.

Drafting company press releases.

Securing articles about the company in newspapers, magazines, online venues, or securing television or media interviews.

Introducing the company to high-net worth individuals.

Introducing the company to investment firms (including, so-called “family offices”).

One IR firm may NOT actually offer all of the above services. In fact, your company may not need all of these services. It is remarkable how often it turns out that a particular IR firm that is heavily courting your company does not provide the services your company actually needs. Hence, as the CEO or CFO — you need to be thoughtful about which of these services your company actually needs and compare that list to the services the firm actually provides.

The next question for examination is: which of the services above are actually effective in bringing your company to the attention of retail investors who might actually purchase your company’s shares through the open market? Be aware that IR firms typically do not work on a contingency basis and expect to be paid a monthly cash retainer (and perhaps an additional equity “kicker”); hence, you will want tangible and measurable value from hiring an IR firm.

Different people have different views of the efficacy of the services noted above in increasing sustained, significant stock trading liquidity. See below for my opinion as to which of the aforementioned services are effective at creating sustained, significant stock trading liquidity for a currently illiquid company stock:

No.

No.

No — unless the company convenes such meetings with hundreds of potential retail investors and has effective phone follow-up.

Unlikely.

Yes, if enough potential retail investors are contacted.

Yes.

No.

This is a good start – an article in USA Today obviously is more valuable than an article in the local newspaper and an appearance on the Fox Business channel is more valuable than an appearance on local news.

Typically not, as the high net worth individual typically would not want to invest in the company through the open market because of the stock illiquidity, although the introduction might result in a direct capital investment or the investor might prefer to wait until the company has sustained, significant trading volume.

No — and a special word of CAUTION. As illuminated in one of my earlier articles, investment firms will NOT invest in a company whose shares do not have sufficient trading liquidity. Hence, if your company has insufficient trading liquidity to attract investment firm capital and an IR firm proposes to introduce your company to investment firms (including, “family offices”), your company is either (a) wasting its time/money or (b) the investment firm will be offering you a “toxic” financing (a topic of a future article).

In sum, as a practical matter, a “mosaic” of the “yes” activities are usually necessary to attract retail investors in sufficient quantity to create sustained and sufficient trading volume to attract investment firm capital. Further, some of the “no” activities have value as well; they simply do not have material value in creating sustained, significant stock trading volumes.

There are dozens of reputable IR firms. Caveat emptor: there are also many more that are disreputable or reputable, but ineffective.

Generating sustained, significant trading volume is a combination of art and science, similar to creating and executing an effective investment “pitch.” What works for one company will not necessarily work for another.

Good luck! Connect with me through Linked In if you have questions.

Up next: Beware the short-seller attack and “bear raids.”

[1] See the article here (stock liquidity necessary to attract investment firm capital) and here (stock liquidity necessary to attract investment analyst coverage).

[2] The article here explains how to estimate the trading volume that will be necessary to attract any particular amount of investment firm capital.

[3] An earlier article illuminated that stock trading liquidity is a necessary, but not sufficient condition, for an investment firm to consider making an investment. In addition to stock liquidity, the company typically must have a compelling business model, large market opportunity, credible management, excellent products, etc.

+++++++++++++++++++++++++++++++++++++++++++++++++

Mr. Woessner mentors and advises companies in the start-up and smaller-cap company ecosphere and helps them raise capital. He also advocates in Washington DC for policies that create a more hospitable public company environment for smaller-cap companies, enhance capital formation, support small business, promote entrepreneurship, and increase upward mobility for all Americans, particularly minorities. See here for more information on Mr. Woessner’s background.

Investment Analysts Typically Do Not Cover Smaller-Cap Illiquid Stocks

In my previous articles, I’ve discussed the issues driving the disappearance of small-cap public companies in the US market. Another example of the in-hospitability of the capital markets to smaller-cap companies is that investment analysts typically do not cover them.[1] According to a 2017 OTC markets survey, 68% of OTC issuers surveyed said they do not have any investment analyst coverage. Similarly, 62% of NASDAQ companies with market capitalizations under $50M do not have any investment analyst coverage.

This lack of investment analyst coverage negatively impacts these companies since academic studies have shown that when an analyst initiates coverage on an issuer its share price increases and its stock trading liquidity increases.

Keep in mind, there are two types of investment analysts: “buy-side” analysts and “sell-side” analysts. A buy-side analyst typically works for an investment fund/institutional investor and writes research reports on issuers whose stock the investment fund/institutional investor is considering purchasing. A sell-side analyst typically works for an investment banking firm and writes research reports on issuers who the analyst believes is an attractive investment opportunity. The report is then distributed to investment funds/institutional investors with the hope they will generate trading commissions for the investment banking firm by purchasing the stock of the issuer that is the subject of the research report.

This article focuses on sell-side analysts, as buy-side analysts do not distribute their reports.

So, why do so few sell-side investment analysts cover illiquid, smaller-cap company stocks?[2]

Because, as explained below, the analyst’s investment banking firm employer typically is not able to monetize a research report covering an illiquid, smaller-cap company.

The analyst’s investment banking firm employer wants to reduce the “overhead expense” of the analyst by having the analyst generate revenue. Hence, the analyst provides the research report to various investment fund/institutional investors with the hope (expectation) that they will initiate a trade in the subject issuer and thereby generate trading commissions for the banking firm.

However, there are NO trading commissions to be made by the analyst’s employer if the analyst’s report covers an illiquid, smaller-cap company because, as explained in an earlier article, investment firms typically do not invest in illiquid, smaller-cap company stocks.

Since there is nil financial gain to the investment banking firm for the investment analyst to write a research report on smaller-cap companies, these research reports typically are not written. Rather, research reports ARE written on companies that have a higher likelihood of generating trading commissions, i.e., those with sufficient trading liquidity to attract investment firm capital.

It was said back in ancient times that “all roads lead to Rome.” For smaller-cap companies — all “roads” to attract investment firm capital require stock trading liquidity.

Not All Stock Investment Analysts are Created Equal

Naturally, an issuer wants to attract investment analysts to cover its stock to increase its stock trading liquidity and its stock price.

Beware: all investment analyst reports are NOT created equal!

Some say that the “buy” or “hold” recommendations issued by sell-side investment analysts are “skewed” to the positive for the purpose of pleasing the issuer about whom the analyst’s report is written. These critics note that approximately less than 7% of sell-side investment analyst ratings are “sell,” with the remainder being “buy” or “hold” or equivalent.

According to these critics, the investment analyst’s employer (typically an investment banking firm) wants to be hired (or continue to be hired) to perform corporate finance activities for the issuer (raising capital, mergers & acquisitions, etc.). They posit that a company is less likely to do business with an investment banking firm whose investment analyst recommends “sell” on its stock. Common sense suggests they are correct.

On the other hand, SEC Regulation AC requires that an investment analyst certify that the views expressed in the report accurately reflect the analyst’s personal views. Hence, an investment analyst’s report presumptively is free of the skewed bias alleged by critics. There is also a so-called “Chinese Wall” between an investment banking firm’s investment analyst department and the firm’s investment banking department to insulate the investment analysts from being influenced by the firm’s investment banking activities.

Commentators have differing views as to the efficacy of these regulatory safeguards.

Academics have studied the efficacy of investment analyst research. These academics have divided sell-side investment analysts into four categories.[3]

These four categories are:

Analysts affiliated with investment banking firms that had NOT done a corporate finance “deal” for the covered issuer within the past year.

Analysts that write research reports for a fee paid by the covered issuer.

Analysts affiliated with investment banking firms that HAD done a corporate finance “deal” for the covered issuer within the past year.

Reports issued by brokerage/independent research firms.

Not surprisingly, the study concluded that reports of analysts in category (1) were perceived as more credible to investors than the reports of analysts in category (3) and, hence, were more effective in increasing the covered issuer’s stock price and increasing the stock’s trading liquidity.

The reports of analysts in category (3) typically are viewed skeptically because the investment banking firm employer had done corporate finance work for the covered company within the prior year (and likely collected a hefty fee). No surprise here.

NOTE: I am NOT saying to reject the offer of an investment analyst report in category (3). If an issuer has the chance to obtain an investment analyst report, typically the issuer should take it.[4]

What does surprise many is that the study concluded that research reports written by investment analysts in category (2) were equally as effective in increasing stock price and stock trading liquidity as the reports of the so-called “unbiased” investment analysts in category (1).

This study’s conclusion is surprising to many because they have the preconception that reports written by analysts in category (2) will be viewed skeptically by investors because the issuer is paying for the report. For this reason, many CEOs and CFOs are hesitant to pay for investment analysts to write a report on their companies. In the face of this academic research, perhaps they should reconsider!

The research reports of firms in category (4) were determined to be equally as ineffective as the research reports in category (3).

There are several firms in category (2) who provide “paid for” investment analyst research reports. They can be located via Internet search. If you contact me through LinkedIn, I can introduce you to some I am aware of.

Next up: How does a company WITHOUT investment analyst coverage obtain such coverage?

What can a company do to increase the trading liquidity of its stock?

The next article discusses increasing your company’s stock trading liquidity with the assistance of an investor relations firm.

[1] This is a “truism” well-documented by a number of sources, including on pages 37 – 38 of the US Treasury 2017 Capital Markets Report available at this link.

[2] An investment analyst will often initiate coverage on a company for whom the analyst’s investment banking firm employer has raised capital or performed other corporate finance activity. As illuminated below, reports of these analysts are often viewed skeptically by investors.

[3] “The First Analyst Coverage of Neglected Stocks, Cem Demiroglu, Michael Ryngaert (2010). The study’s conclusions appear on pages 555 – 558 and 581 – 582.

[4] The reasons are beyond the scope of this article.

Mr. Woessner mentors, advises, and raises capital for companies in the start-up and smaller-cap company ecosphere. He also advocates in Washington DC for policies that create a more hospitable public company environment for smaller-cap companies, enhance capital formation, support small business, promote entrepreneurship, and increase upward mobility for all Americans, particularly minorities. For more information on Mr. Woessner’s background, see the link here.

US public companies are disappearing! This trend is 100% opposite the trend in other developed countries with similar institutions and economic development.

Many private companies avoid going public, preferring instead to “exit” their investment by selling the company, or hold off going public as long as they can.

This trend is causing US public companies to disappear. For example, US public company listings decreased over the last two decades by about 46%, from 8,090 in 1996 to 4,331 in 2016, according to a 2018 academic study from the Harvard Kennedy School.[1]

Conversely, public company listings increased by about 48% in other developed countries over a comparable period, according to another academic study in 2015. According to that study, the US “should have had” approximately 9,500 public companies in 2012, resulting in an estimated “listing gap” of approximately 5,400 companies as of 2012. The listing gap is undoubtedly higher today.

This disappearing public company trend has profoundly negative consequences for US job growth. A March 2011 report from the Department of the Treasury’s “IPO Task Force” determined that 92% of the job growth among companies who had gone public occurred after the company’s IPO.

Another negative consequence of the disappearing public company is that as public companies disappear, there are fewer public companies for mutual funds (Vanguard, Fidelity, etc.), pension funds, and the like to invest in. If current trends continue, the “S&P 500” will become the “S&P 250.”

Moreover, not only does staying private thwart US job growth, it deprives mom-and-pop “Main Street” investors of opportunities to invest at the early stage of a business and reap significant gains in value during the business’ early, private years.

To wit, Uber and AirBnB are two well-known companies that have not yet gone public and whose investors (principally Silicon Valley and Wall Street investment firms and high-net worth individuals) are poised to make HUGE sums of money on their investments. In this regard, note the recent news reports that Uber’s proposed IPO market valuation is $120 BILLION. “Main Street” investors will made ZERO from the success of these (and similar) venture capital funded companies because these investment opportunities and similar ones are not made available to them. This statement is not a criticism of the investors who stand to make an enormous amount of money (after all they took a risk with their money and are entitled to a return) – it is simply a statement of fact.

As a counterweight to this trend of income being redistributed to Silicon Valley and Wall Street investment firms and high-net worth individuals, SEC Chairman Jay Clayton wants to let more “Main Street” investors participate in private deals. Within recent months he was quoted in The Wall Street Journal as saying:

Many companies have shunned the public markets in favor of private investors,

Regulators have for decades typically walled off most private deals from smaller investors, who must meet stringent income and net worth requirements to participate,

The SEC is now weighing a major overhaul of rules intended to protect mom-and-pop investors, with the goal of opening up new investment options for them.

We thank Chairman Clayton for recognizing the need for SEC policies that permit more Main Street investors to invest in private deals. But — permitting more Main Street investors to invest in privatedeals does NOT fix the problem of the declining number of US public companies.

CAUSES OF THE “DISAPPEARING” US PUBLIC COMPANY

So, what is behind the precipitous fall in the numbers of US public companies over the past decades? The following factors have played a significant role in this alarming trend:

More and more companies are turning to the private markets for their capital needs. According to a 2017 Report by the Department of the Treasury, from 2012 through 2016, the debt and equity capital raised through private offerings was 26% higher than that raised through the public markets.

Smaller-cap companies are not going public. The small (less than $50M – $100M) IPO has practically disappeared. The number of small IPOs averaged 401 in the 1990s, but then dropped to only 105 annually in the 18 years since. In the 1990s, small IPOs comprised 27% of capital raised in the public markets, whereas in the period from 2000 to present they have comprised only 7% of all capital raised. In fact, research shows that the collapse of the smaller IPOs is ~100% responsible for the listing gap between the current number of US public companies and the number of public companies the US “should have.”

Why are smaller-cap companies not going public or delaying going public until they are larger-cap companies? Answer: because the public company ecosphere is “inhospitable” to smaller-cap public companies, as evidenced by the below:o Regulatory requirements of Sarbanes – Oxley and Dodd-Frank are burdensome

o Smaller-cap companies are vulnerable to “bear raid” attacks by short sellers

o There is little to no sell-side investment analyst coverage

o Buy-side investing trends have changed whereby retail investors are moving to mutual funds, rather than investing in individual stocks

o The threat of class-action lawsuits is a deterrent

o The public company reporting (Form 10Q, 10K, 8K) requirement is a deterrent

As if the preceding reasons were not deleterious enough: public markets also are inhospitable to smaller-cap companies for the following reason: once publicly-traded, the stocks of many smaller-cap companies are likely to be illiquid[2]; and for companies with an illiquid stock, it is virtually impossible to raise non-toxic capital from investment firms because investment firms are reluctant to invest in smaller-cap, illiquid stocks.[3]

Private company CEOs and CFOs look at all of these in-hospitability factors and determine they simply don’t want to be a public company.

Despite the foregoing, smaller-cap companies can thrive in the public markets. If you are a CEO or CFO of a smaller-cap company with an illiquid stock and your company is struggling to raise non-toxic capital => don’t despair! A subsequent article will provide you specific, actionable recommendations for increasing your company’s stock liquidity.

Subsequent articles will also unveil a policy solution that, if implemented, will reverse the trend of The “Disappearing” US Public Company!

[2] According to a 2018 SEC study of thinly-traded securities, 3,500 of 8,700 NMS-traded securities had a dismal, median average daily volume of < 50,000 shares per day.The trading volumes of OTC-traded stocks are even more dismal. A subsequent article will provide more detail regarding these dismal trading volumes.

[3] Lack of trading liquidity makes it virtually impossible for investment firms initially to invest through the open market without affecting the stock price – similarly, lack of liquidity makes it virtually impossible for them to exit an investment position through the open market. See an earlier article here that addresses this topic in more detail.

This is a reprint of an article by Mr. Woessner published on December 12, 2018 by equities.com at this link.

Mr. Woessner mentors, advises, and helps raise capital for companies in the start-up and smaller-cap company ecosphere. He also advocates for policies to help smaller-cap companies access capital and for policies that create a more hospitable public company environment for them. For more information on Mr. Woessner’s background, see https://www.linkedin.com/in/ronald-woessner-3645041a/.

This article explains how Dodd-Frank crushed the ability of publicly-held[1], smaller-cap companies to raise capital. The unintended consequences of government regulation on the financial markets has taken a disproportionate toll on the small-cap market for decades, and has transformed what once was a vibrant, robust driver of the economy into a shell of its former self. Dodd-Frank has exacerbated this problem, further stifling emerging growth opportunities for startups and small-cap companies by restricting their access to capital, resulting in an increasingly top-heavy market.

The chart below, excerpted from an article by noted financial analyst Michael Markowski, who predicted the demise of Lehman, Bear Stearns and Merrill Lynch, illustrates that the Dodd-Frank legislation crushed the valuations of smaller-cap companies, in addition to dampening economic growth, creating higher unemployment and its many other documented harms to the US economy.

This in turn crushed the ability of smaller-cap companies to raise capital and obtain funding from sources other than Founders and Friends & Family investors.

The crushing of smaller-cap company valuations by Dodd-Frank led to other consequences for this asset class, and resulted in investment firms becoming more unwilling to invest in smaller cap companies.

To illuminate those steps smaller-cap companies can take to create access to investment firm capital in this ecosphere (which will be discussed in subsequent articles(, we first must understand the specific challenges these companies are facing under Dodd-Frank.

Why It Is Difficult for Smaller-Cap Companies to Raise Capital

Here are the typical sources of investment capital for start-up/emerging companies:

Personal Loans/Credit of Founders – fund 57% of start-ups

Friends & Family – fund 38%

Venture Capital Funds – fund .05%

Angel Investors – fund .91%

“JOBS 1.0 Act” Crowdfunding – not yet a significant capital source

As can be seen, venture capital funds and angel investors fund less than 1% of start-up/emerging companies in the US. Hence, unless your company is one of those companies that fits the specific company profile that venture capital firms or angel investors are seeking, your chances of raising capital from a venture capital firm or angel investor approach ZERO.

Rather, as the metrics above reveal, “Personal Loans/Credit of Founders” and “Friends & Family” provide the preponderance of capital for start-up/emerging companies. Of course, the capital of Founders and Friends & Family can become “tapped out” as not many of us entrepreneurs are wealthy or are fortunate enough to have wealthy friends willing to invest material amounts of capital in our business ventures.

As these capital sources become “tapped” out, our companies need to attract alternate sources of capital, such as investment firms (including family offices). Access to these alternate sources of capital is needed for our start-up/emerging companies to thrive or even survive.

Unfortunately, unless your business operates in a “hot sector,” such as biotech, cannabis, digital currency or whatever the hot sector trend happens to be during the market cycle when you are seeking capital, investment firms typically will not invest in your start-up/emerging ventures for a number of reasons.

One reason is because investment firms want to invest in asset classes that are increasing in value, and not those decreasing in value. Yet, the valuations of these companies have been crushed by Dodd-Frank, as previously noted. This creates a death spiral scenario for companies of this type.

Common sense informs us that since smaller-cap company valuations have decreased in value relative to other asset classes, it will be more difficult for smaller-cap companies to attract investment firm capital.

Further, this Dodd-Frank crushing of smaller-cap company valuations has not only crushed the ability of smaller-cap companies to raise capital it has also virtually killed the stock trading liquidity (i.e., number of shares traded daily through the public markets) of the smaller-cap company market segmentThis has created a downward “death spiral” of the trading price and trading volume for many publicly-traded smaller-cap company stocksThis downward “death” spiral looks like this

If the value of an asset class has been crushed — as DF has done to smaller-cap company shares — relative to alternative asset classes, there is less demand for that asset class

Less demand results in a lower trading volume

Lower trading volume results in a lower price (Economics 101: law of supply/demand)

Lower price s then leads to lower trading volume, which results in lower prices , which results in a lower trading volumes, and so forth as the death spiral cycle repeats

This vicious downward “death spiral” ensues in both stock price and trading volume.

Lower Trading Volume then results in ZERO Institutional Investment

Investment firms typically are unwilling to invest in companies that have low trading volumes.

Why?

See below for an investment firm’s calculus relating to its evaluation of potential investment candidates, which illuminates why investment firms typically are unwilling to invest in smaller-cap company stocks:

The amount invested must be sizeable enough to “matter” for the investment firm

Let’s assume $2 million in capital is to be invested by the investment firm

The firm typically seeks to complete its investment within one month (20 trading days)

$2 million to be invested, divided by 20 trading days = $100,000 per day invested

The firm typically does not want its stock purchases to drive up the stock trading price, which would result in the firm’s paying more for the stock, so it typically seeks to limit its purchases to < 10 – 15% of daily trading volume so as not to drive up the stock price

To invest $100,000 per day within the 10 – 15% parameter means there must be a daily trading volume of between $667,000 – $1 million

Moreover, even if the investment firm is able to take an investment position in the stock, they will be concerned they cannot readily exit their investment position. Some have used the “Hotel California” metaphor: “You can check out any time you like, But you can never leave!”

Bottom line: companies WITHOUT the requisite trading volume will NOT receive investments from investment firms, regardless of how much the firm might otherwise like the company.

Former institutional small-cap investor Adam J. Epstein has written a book, The Perfect Corporate Board: A Handbook for Mastering the Unique Challenges of Small-Cap Companies, available on Amazon at this link, which has a more fulsome discussion of this topic.

Summary

In sum, Dodd-Frank’s killing of stock trading volumes of smaller-cap public companies has made it virtually impossible for many of them to raise investment firm capital, which cripples or even kills the company because as noted above, once a smaller-cap company runs out of Founder and Friends/Family money, they have virtually no where to go for capital.

But all is not lost – my subsequent articles will illuminate what can be done to overcome the effect of Dodd-Frank!

[1] While the focus of this article and others is this series is publicly-held, smaller-cap companies, many of the same principles apply to private companies.

This is a reprint of an article by Mr. Woessner published on December 4, 2018 by equities.com at this link.

Mr. Woessner mentors, advises, and helps raise capital for companies in the start-up and smaller-cap company ecosphere. He also advocates for policies to help smaller-cap companies access capital and for policies that create a more hospitable public company environment for them. For more information on Mr. Woessner’s background, see https://www.linkedin.com/in/ronald-woessner-3645041a/.

See below for an article by Cromwell Coulson, President, CEO and Director of OTC Markets Group, regarding “Understanding Short Sale Activity.”

Quality data is essential to well-functioning markets. Improving the availability, relevance and usefulness of data aligns with OTC Market Group’s mission to create better informed, more efficient financial markets. In our experience, short selling remains one of the most highly-debated topics among academics, companies, investors, market makers and broker-dealers. As a market operator and company CEO, I believe it’s critical to address the misconceptions that still exist around short sale data and the correlation to a stock’s fundamental value.

Short selling, the sale of a security that the seller does not own, has long been a controversial practice in public markets. Advocates for short selling believe it builds price efficiency, enhances liquidity and helps improve the public markets, while critics are concerned that it can facilitate illegal market manipulation and is detrimental to investors and public companies. Given the diverse range of opinions and opposing views, we believe the first step is to take a deeper dive into the data and help separate out the noise.

“The Reliable” – FINRA Equity Short Interest Data

The most accurate measure of short selling is the data reported by all broker-dealers to FINRA on a bi-weekly basis. These numbers reflect the total number of shares in the security sold short, i.e. the sum of all firm and customer accounts that have short positions.

This information is available on www.otcmarkets.com on the company quote pages. As an example, OTC Markets Group has a few hundred shares sold short on average, which represents a fraction of our daily trading volume and shares outstanding.

OTC Markets Group (OTCQX: OTCM) SHORT INTEREST Data

DATE

SHORT INTEREST

PERCENTAGE CHANGE

AVG. DAILY SHARE VOL

DAYS TO COVER

SPLIT

NEW ISSUE

9/28/2018

97

11.49

5,551

1

No

No

9/14/2018

87

8.75

4,423

1

No

No

8/31/2018

80

100.00

6,818

1

No

No

7/31/2018

103

-48.24

3,197

1

No

No

7/13/2018

199

-27.64

2,124

1

No

No

6/29/2018

275

166.99

3,239

1

No

No

6/15/2018

103

24.10

2,739

1

No

No

5/31/2018

83

-72.33

3,925

1

No

No

5/15/2018

300

1.69

3,944

1

No

No

4/30/2018

295

100.00

4,278

1

No

No

FINRA Rule 4560 requires FINRA member firms to report their total short positions in all over-the-counter (“OTC”) equity securities that are reflected as short as of the settlement date. In 2012 FINRA clarified that firms must report short positions in each individual firm or customer account on a gross basis under FINRA Rule 4560. Therefore, firms that maintain positions in master/sub-accounts or parent/child accounts must calculate and report short interest based on the short position in each sub- or child account.

Since this data is part of a clearing firm’s books and records, it is of high quality and FINRA regularly inspects broker-dealer compliance with the rule. Of course, it would be great if this data was collected and published daily (with an appropriate delay).

“The Misleading” – Daily Short Volume

In contrast, the most frequently misinterpreted data is the Daily Short Volume, sometimes referred to as Naked Short Interest. This data shows the percentage of published trade reports (called media transactions in FINRA Rules) that were marked short. As an example, the recent data for OTC Markets Group shows that up to 90% of the trading volume comes from short

selling on some days. If we did not carefully track our bi-weekly Short Interest, we could easily be led to believe that short selling is rampant in our stock.

Historical Short Volume Data for OTC Markets Group (OTCQX: OTCM)

DATE

VOLUME

SHORT VOLUME

PERCENTAGE of VOL SHORTED

Oct 18

3,341

1,399

41.87

Oct 17

5,989

3,198

53.40

Oct 16

16,120

7,509

46.58

Oct 15

24,155

12,991

53.78

Oct 12

6,297

4,914

78.04

Oct 11

4,059

1,553

38.26

Oct 10

2,185

999

45.72

Oct 9

7,473

4,556

60.97

Oct 5

880

525

59.66

Oct 4

492

200

40.65

Oct 3

2,041

801

39.25

Oct 2

4,786

1,560

32.60

Oct 1

3,973

2,607

65.62

Sep 28

244

23

9.43

Sep 27

882

805

91.27

Sep 26

259

189

72.97

Sep 25

3,085

2,250

72.93

Sep 24

967

571

59.05

Sep 21

2,350

825

35.11

Sep 20

7,164

6,453

90.08

Sep 19

297

202

68.01

Seeing the above data can be alarming for public companies and their investors, until they understand the inner workings of how dealer markets function and broker trades are reported—which render the data virtually meaningless.

Since this data also comes from FINRA, what gives? The daily short selling volume is misleading because market makers and principal trading firms report a large number of trades as short sales in positions that they quickly cover. For market makers with a customer order to sell, they will temporarily sell short (which gets published to the tape as a media transaction for public dissemination) and then immediately buy from their customer in a non-media transaction that is not publicly disseminated to avoid double counting share volumes. SEC guidance also mandates that almost all principal trading firms that provide liquidity at multiple price levels, or arbitrage international securities, must mark orders they enter as short, even though those firms might also have strategies that tend to flatten by end of day. Since the trade reporting process for market makers and principal trades makes the Daily Short Volume easily misleading, we do not display it on www.otcmarkets.com.

Making daily short reporting data easily-digestible and relevant is not hard. On the contrary, it should be easy to aggregate all of the short selling that is reported as agency trades, as well as all of the net sum of buying and selling by each market maker and principal trading firm. This would paint a clear picture for investors of overall daily short selling activity. Fixing the misleading daily short selling data would bring greater transparency and trust to the market.

“The Missing Piece”– Short Position Reporting by Large Investors