This in turn crushed the ability of smaller-cap companies to raise capital and obtain funding from sources other than Founders and Friends & Family investors.

The crushing of smaller-cap company valuations by Dodd-Frank led to other consequences for this asset class, and resulted in investment firms becoming more unwilling to invest in smaller cap companies.

To illuminate those steps smaller-cap companies can take to create access to investment firm capital in this ecosphere (which will be discussed in subsequent articles(, we first must understand the specific challenges these companies are facing under Dodd-Frank.

Why It Is Difficult for Smaller-Cap Companies to Raise Capital

Here are the typical sources of investment capital for start-up/emerging companies:

Personal Loans/Credit of Founders – fund 57% of start-ups

Friends & Family – fund 38%

Venture Capital Funds – fund .05%

Angel Investors – fund .91%

“JOBS 1.0 Act” Crowdfunding – not yet a significant capital source

As can be seen, venture capital funds and angel investors fund less than 1% of start-up/emerging companies in the US. Hence, unless your company is one of those companies that fits the specific company profile that venture capital firms or angel investors are seeking, your chances of raising capital from a venture capital firm or angel investor approach ZERO.

Rather, as the metrics above reveal, “Personal Loans/Credit of Founders” and “Friends & Family” provide the preponderance of capital for start-up/emerging companies. Of course, the capital of Founders and Friends & Family can become “tapped out” as not many of us entrepreneurs are wealthy or are fortunate enough to have wealthy friends willing to invest material amounts of capital in our business ventures.

As these capital sources become “tapped” out, our companies need to attract alternate sources of capital, such as investment firms (including family offices). Access to these alternate sources of capital is needed for our start-up/emerging companies to thrive or even survive.

Unfortunately, unless your business operates in a “hot sector,” such as biotech, cannabis, digital currency or whatever the hot sector trend happens to be during the market cycle when you are seeking capital, investment firms typically will not invest in your start-up/emerging ventures for a number of reasons.

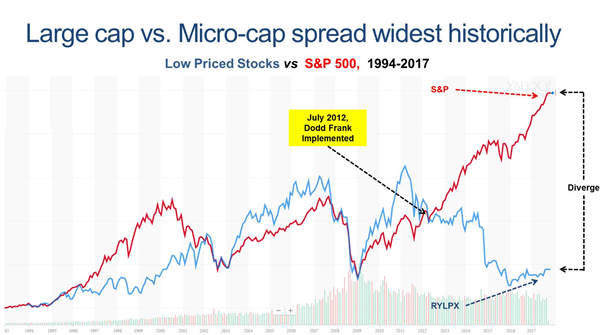

One reason is because investment firms want to invest in asset classes that are increasing in value, and not those decreasing in value. Yet, the valuations of these companies have been crushed by Dodd-Frank, as previously noted. This creates a death spiral scenario for companies of this type.

Common sense informs us that since smaller-cap company valuations have decreased in value relative to other asset classes, it will be more difficult for smaller-cap companies to attract investment firm capital.

Further, this Dodd-Frank crushing of smaller-cap company valuations has not only crushed the ability of smaller-cap companies to raise capital it has also virtually killed the stock trading liquidity (i.e., number of shares traded daily through the public markets) of the smaller-cap company market segmentThis has created a downward “death spiral” of the trading price and trading volume for many publicly-traded smaller-cap company stocksThis downward “death” spiral looks like this

- If the value of an asset class has been crushed — as DF has done to smaller-cap company shares — relative to alternative asset classes, there is less demand for that asset class

- Less demand results in a lower trading volume

- Lower trading volume results in a lower price (Economics 101: law of supply/demand)

- Lower price s then leads to lower trading volume, which results in lower prices , which results in a lower trading volumes, and so forth as the death spiral cycle repeats

This vicious downward “death spiral” ensues in both stock price and trading volume.

Lower Trading Volume then results in ZERO Institutional Investment

Investment firms typically are unwilling to invest in companies that have low trading volumes.

Why?

See below for an investment firm’s calculus relating to its evaluation of potential investment candidates, which illuminates why investment firms typically are unwilling to invest in smaller-cap company stocks:

- The amount invested must be sizeable enough to “matter” for the investment firm

- Let’s assume $2 million in capital is to be invested by the investment firm

- The firm typically seeks to complete its investment within one month (20 trading days)

- $2 million to be invested, divided by 20 trading days = $100,000 per day invested

- The firm typically does not want its stock purchases to drive up the stock trading price, which would result in the firm’s paying more for the stock, so it typically seeks to limit its purchases to < 10 – 15% of daily trading volume so as not to drive up the stock price

- To invest $100,000 per day within the 10 – 15% parameter means there must be a daily trading volume of between $667,000 – $1 million

Moreover, even if the investment firm is able to take an investment position in the stock, they will be concerned they cannot readily exit their investment position. Some have used the “Hotel California” metaphor: “You can check out any time you like, But you can never leave!”

Bottom line: companies WITHOUT the requisite trading volume will NOT receive investments from investment firms, regardless of how much the firm might otherwise like the company.

Former institutional small-cap investor Adam J. Epstein has written a book, The Perfect Corporate Board: A Handbook for Mastering the Unique Challenges of Small-Cap Companies, available on Amazon at this link, which has a more fulsome discussion of this topic.

Summary

In sum, Dodd-Frank’s killing of stock trading volumes of smaller-cap public companies has made it virtually impossible for many of them to raise investment firm capital, which cripples or even kills the company because as noted above, once a smaller-cap company runs out of Founder and Friends/Family money, they have virtually no where to go for capital.

But all is not lost – my subsequent articles will illuminate what can be done to overcome the effect of Dodd-Frank!

[1] While the focus of this article and others is this series is publicly-held, smaller-cap companies, many of the same principles apply to private companies.

© Ronald A. Woessner, December 2018

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

This is a reprint of an article by Mr. Woessner published on December 4, 2018 by equities.com at this link.

Mr. Woessner mentors, advises, and helps raise capital for companies in the start-up and smaller-cap company ecosphere. He also advocates for policies to help smaller-cap companies access capital and for policies that create a more hospitable public company environment for them. For more information on Mr. Woessner’s background, see https://www.linkedin.com/in/ronald-woessner-3645041a/.